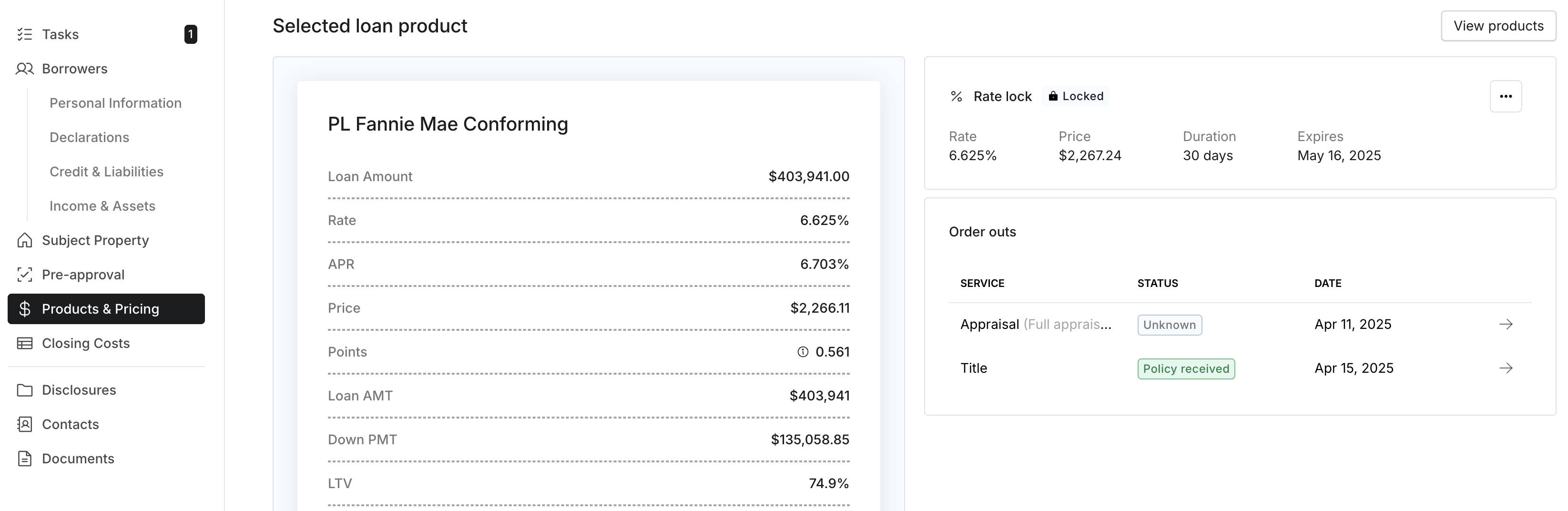

Order Outs

Order Outs

What “order-outs” does Pylon handle?

Pylon manages several key third-party services (“order-outs”) throughout the loan process to streamline operations and reduce manual work for LOs.

Here’s a breakdown:

Appraisal: Ordered by Pylon. The cost is paid by the borrower at closing; if the loan does not close, Pylon absorbs the cost.

Title: Ordered by Pylon when using a preferred title company. If using a borrower’s chosen title company (common in purchases), the LO/borrower must coordinate directly and upload required documents.

Verification of Employment (VOE): Handled by Pylon, including manual VOEs when not completed through Truv.

How are appraisals ordered in Pylon?

The appraisal is ordered as soon as the borrower signs the Intent to Proceed (ITP) and the file moves into the Processing status. For purchase transactions, the executed purchase contract must also be on file before the order can proceed.

Appraisals can be managed directly within the “Products & Pricing” section of the Command Center under “Order Outs.”

Here’s how the process works:

Pylon orders the appraisal automatically on behalf of the borrower.

Pylon covers the cost upfront.

The borrower pays for the appraisal at closing.

How does Pylon's AMC network work, and can specific appraisers be added?

Pylon uses a network of AMCs assigned based on geography. Specific appraisers can be added to extend coverage (particularly for rural areas). To request an appraiser be added, provide their name, email, phone number, and license information to your account contact.

Does Pylon accept ACE (Automated Collateral Evaluation) with a PDR (Property Data Report) for Freddie Mac loans?

Yes.

Can an appraisal be transferred out of Pylon to another lender?

Yes. Pylon will transfer an appraisal to another lender. The borrower must first pay for the appraisal via a payment link provided by Pylon. Once payment is confirmed, Pylon sends the receiving lender the transfer letter, appraisal (PDF and XML), SSRs, invoice, and AIR Certification. To initiate an outbound transfer, contact sean@pylonlending.com (Sean VanCoutren) with the file number.

Can an appraisal be transferred into Pylon from another lender?

Yes. Pylon accepts appraisal transfers in. The prior lender must provide: the appraisal report (PDF and XML), SSRs, AIR compliance certification, invoice, and a transfer letter. To initiate an inbound transfer, submit a support ticket with the file number; the receiving contact at Pylon is sean@pylonlending.com (Sean VanCoutren). Register the loan in Command Center before initiating the transfer.

Can an appraisal be requested as a rush, with a higher disclosed appraisal fee?

Yes. Rush appraisal requests can be accommodated; reach out via the support process with the file number to coordinate the higher fee disclosure.

How are title services ordered in Pylon?

Title ordering can be managed directly within the “Products & Pricing” section of the Command Center under “Order Outs.”

Here’s how the process works:

Title ordering begins after the borrower signs the Intent to Proceed (ITP). There are two possible pathways depending on whether the borrower uses Pylon’s preferred title provider or selects their own.

Option 1: Pylon’s Preferred Title Company

If no preference is confirmed, Pylon will order title through its preferred provider.

Pylon handles the full process.

Option 2: Borrower’s Chosen Title Company

The Loan Officer must confirm whether the borrower has a preferred title company.

If so, the LO should request the following from the title company:

Title Commitment

Closing Protection Letter (CPL)

Tax Certificate

Wire Instructions

Title E&O Policy

Fee Sheet

All documents must include the loan number and correct mortgagee clause, and be uploaded into Command Center for review.

Mortgagee Clause: Pylon Lending, ISAOA 215 Park Avenue South, Floor 11 New York, NY 10003.

Important Notes:

LOs will receive a task to confirm title preference.

If no preference is confirmed within 7 days, Pylon will proceed with ordering title through its preferred provider.

To avoid duplicate orders or cancellations (especially on purchase transactions), confirm the borrower’s preference as early as possible.

How is the condo questionnaire handled, and who covers the cost?

The loan officer should obtain the condo documents, including the questionnaire. Pylon reviews and approves the documentation as part of underwriting. The Condo Certification fee is collected from the borrower at closing.